Trading companies and manufacturing companies usually have a warehouse or distribution centre. Raw materials and supplies, intermediate products, semi-finished products, finished products and spare parts are stored there. The storage of these goods causes costs, the totality of which is referred to as storage maintenance costs, warehousing costs or storage costs, which in turn make up a large part of the logistics costs.

A distinction is made between two types of storage maintenance costs: on the one hand, the costs that are directly linked to the warehouse and, on the other hand, the interest costs for the capital tied up in the inventory. Interest gains are lost here and thus do not contribute to the increase in capital. Such costs are referred to as opportunity costs. In accounting terms, storage maintenance costs are usually included in distribution costs, except when storage contributes to the production process, such as in the fermentation of alcoholic beverages -in which case storage maintenance costs are included in production costs. The amount of warehousing costs depend on many factors, but it can be said that the lower the degree of automation and rationalisation in the warehouse, the higher they are.

Components of storage maintenance costs

Many individual items together make up the storage maintenance costs. Depending on your point of view, they can be divided and assigned differently.

- The costs of storage capacity

This includes the warehouse building itself, the storage facilities, such as shelving systems, the means of warehouse transport, such as shelf conveyors and forklifts, and the costs for warehouse personnel.

- The costs of storage itself

The stored goods must be preserved quantitatively and qualitatively. An example is foodstuffs, where conservation costs are incurred. In addition, interest costs are incurred on the capital tied up in inventories, so-called imputed interest.

- The costs of readiness for storage

This includes maintenance costs as well as the costs for lighting, cooling and heating.

- The costs of warehouse preparation and post-processing

The storage, relocation and retrieval of materials cause costs, for example in the form of fuel and electrical power, for conveyor aids (forklifts, driverless means of transport) and conveyor landscape. The costs for order picking, unpacking and packaging (see also finishing/packing, value-adding processes) are also part of the pre-storage and post-storage work.

Other types of distribution create a different relationship between the individual items; for example, the following super points can be formed with regard to costs in a profitability analysis:

- Storage rooms (rent, maintenance, heating, lighting, water, cleaning, depreciation/impairment, return on capital invested, insurance)

- Goods (interest on capital tied up in stock, shrinkage/wear/spoilage and breakage/damage/theft of goods, storage risk, insurance)

- Subsidies/aids (depreciation, operating costs, repair/maintenance, insurance, forklift trucks, Euro pallets)

- Material costs (packaging material and office material of the warehouse management – see Green Logistic)

Alternatively:

- Storage space (depreciation, interest, buildings, inventory, insurances, rent)

- Inventories (interest, insurance, inventory losses)

- Handling of stocks (transport of goods, operating costs of conveyors, weighing, measuring, mixing, dividing, ventilating, humidifying)

- Warehouse management (personnel costs as well as hardware and software used)

Furthermore, a distinction can be made between fixed and variable costs, as well as between warehousing costs for finished products and for intermediate products. If there are several storage stages, such as goods receipt, production and finished parts storage, then the warehousing costs must be calculated for each stage. Ultimately, the storage maintenance costs can only be accurately recorded and allocated if the locations where the warehouse services are performed are separated and recorded as cost centres or cost locations.

Relevance ofstorage maintenance costs

With numerous logistical decision problems, such as lot size planning (see lot size), or the implementation of logistics concepts, such as just-in-time production, the storage maintenance costs are very important in terms of economic success or failure. Their reduction involves considerable rationalisation potential. The most favourable is the optimum stock level, which lies between too small and too large a stock level. If a stock is too small, machines and personnel are not used to full capacity, while too large stock causes too high, unnecessary costs; both lead to shortage costs. In industry, storage maintenance costs average around 50 per cent of logistics costs; in wholesale and retail, on the other hand, this share is considerably higher—ranging from 60 per cent to 80 per cent of total costs (balance sheet total). The storage of goods, therefore, causes financial costs that must always be carefully weighed against the costs and the risk of delivery delays in order to operate profitably. Storage maintenance costs play a particularly important role in stock-intensive companies. Such companies include all those with a very high share of storage maintenance costs in the total costs or with a considerable share of stock in the total assets—the assets represent part of the company balance sheet, which is used as capital within the company. The company can, therefore, fall back on less money. Such enterprises are mostly found in wholesale, retail and mechanical engineering.

Storage intensity

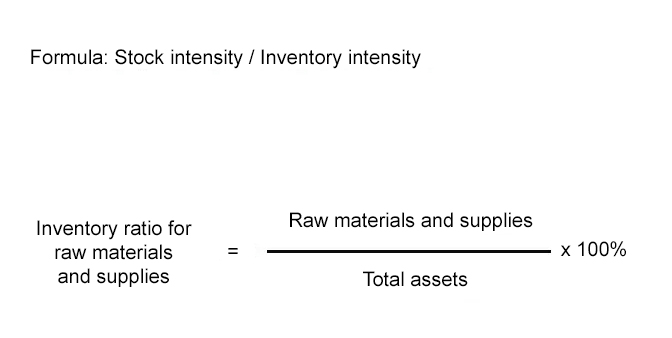

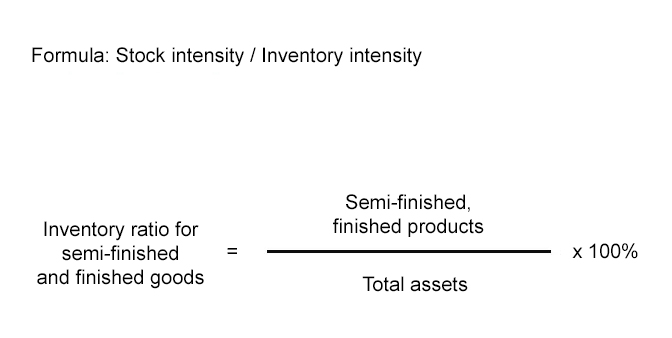

In this context, storage intensity is an important key figure. It is also called stock intensity and expresses how much capital is tied up in the form of warehouse stock. A high capital commitment causes high costs and affects both liquidity and profitability, which is reflected in the inventory intensity by the following formula, for which the following figures from the annual balance sheet are required: Inventories (total value of inventories) and total assets (balance sheet total).

This formula can also be applied explicitly to raw materials, consumables and supplies on the one hand and semi-finished and finished goods on the other. In order for storage maintenance costs to be collected as quickly as possible, the higher the inventory intensity, the greater the inventory turnover rate must be. If the inventory intensity rises, then the causes must be investigated; these can be due to increased production times or poor inventory management or a poorly maintained merchandise management system.

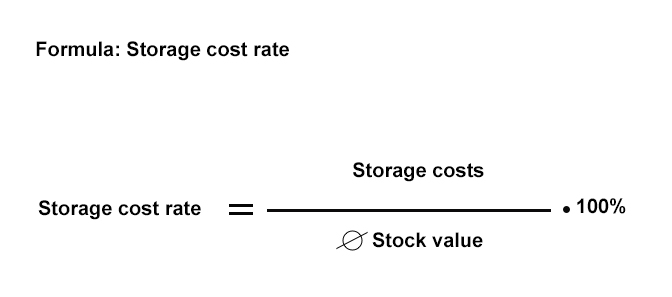

Storage cost rate

Another important key figure is the storage cost rate. Here, the storage maintenance costs are set in relation to the average warehouse stock using the following formula:

The storage cost rate can also be used to calculate the costs per individual stored good. If, for example, the cost price (also the purchase price—in accounting, the price is also the price for merchandise purchased) of a 10-litre bucket of paint is 50 euros and the storage cost rate is 10 per cent, then the warehousing costs per bucket amount to 5 euros (10 per cent of 50 euros) for the corresponding period of the raw data used. The storage maintenance costs are therefore charged as a lump sum to the goods in stock in proportion to the value of the goods. These warehousing costs must be included in the price calculation because if the sales price is too high compared to the competition, the warehousing costs should be reduced, as they make up a considerable part of the total costs.

Cut storage maintenance costs

The storage maintenance costs can be reduced by using several adjusting screws; the main influencing factor is the stock level. In detail, the following optimisation potentials can be assumed:

- Determination of stock levels and relevant key figures as accurately as possible

The correctness and completeness of the inventory results from the corresponding data/information. These can originate from the last inventory and can be merged manually, or an ERP or merchandise management system is used, which continuously evaluates the stock and generates the required key figures. The storage intensity and the storage cost rate are then determined, which provide information on the need for action in a time and industry comparison.

- Inventory cleaning

So-called “slow-moving items” must be determined and, if necessary, eliminated. Before this, however, it must first be defined what a slow-moving item is, which is very sector-and company-dependent. Goods that have been in the warehouse for too long must, therefore, be scrapped, recycled elsewhere, returned or sold in a special sale. Stock clearance is particularly worthwhile for goods with a high stock value (see also stock management), but of course also for goods with a small unit value but a quantitatively large stock.

- Optimisation of Inventory Management

The measure aims to ensure ideal availability for all goods required regularly, without maintaining excessive stocks. For such an analysis, there are systematic procedures (for example ABC analysis), which are usually supported by ERP and merchandise management systems as well as by warehouse management systems (WMS).

- Demand-oriented inventory management

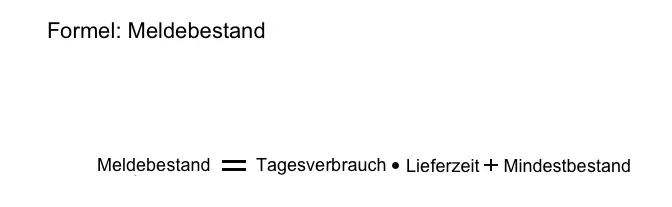

This involves determining the optimum stock level, which can only be sensibly managed from a certain order of magnitude using software solutions. The most important factors are the average consumption, the minimum stock level and the possible maximum stock level (related to the spatial capacity and the capital value) as well as the replenishment time. If these parameters are used, both the optimum stock level and the reorder point (reorder point for replenishment) result. ERP systems perform this calculation regularly, automatically or semi-automatically at certain intervals (for example, weekly).

- Define maximum stock

For goods with a high commodity value, a well-calculated maximum stock level should be defined, as otherwise these would cause a large capital commitment and contribute to correspondingly high warehousing costs. If it is difficult to reduce the maximum stock of such articles because they are consumed very frequently, the delivery times can also be shortened, and the order frequency increased (keyword “demand-oriented delivery”).

- Optimal procurement quantity

Since each purchase order also incurs its own costs, it is advisable to determine the optimum procurement quantity using certain lot-size formulas.

- Optimisation of logistical processes

The logistical processes or process steps in a warehouse also have great potential for optimisation; for example, a storage location system can be introduced, or process and transport routes can be shortened, as is the case with manual sorter picking, for example.

Summary of storage maintenance costs, warehousing costs, storage costs

Storage maintenance costs, storage costs or warehousing costs are all costs incurred that are linked to a warehouse and the corresponding warehouse processes. They are an important part of logistics costs and are used to determine cost-optimised procurement quantities derived from lot-size formulas and key figures. Low storage maintenance costs increase liquidity and are a result of the use of appropriate software solutions and automation measures. In essence, the determination of warehousing costs involves the question of whether it is more cost-effective to procure a large quantity with a high warehouse range or to procure small quantities more frequently in order to keep storage maintenance costs constantly low.

Warehouse management - as simple as possible, as complex as necessary

Our WMS offers you an individually tailored, lean and process-oriented warehouse management.

Also available in Deutsch (German)